Prime Minister Datuk Seri Anwar Ibrahim announced a new e-Invoice Special Voluntary Disclosure Programme on July 7, creating a grace period until the end of 2027 for businesses to update their digital tax records without incurring financial penalties. The initiative represents a significant policy shift aimed at easing compliance burdens, particularly for Malaysia's substantial small and medium-sized business sector, which has faced challenges adapting to the government's mandatory e-invoicing system.

The Inland Revenue Board has structured the programme to accommodate three distinct groups of taxpayers. The first category includes businesses that failed to submit e-Invoices for qualifying transactions within the required timeframe. The second covers organisations that submitted e-Invoices but included errors or omissions that fell short of regulatory specifications. The third and broadest category encompasses any taxpayer who did not lodge e-Invoices for any period dating from when the government first mandated the system's implementation. This expansive scope suggests the IRB recognises widespread compliance difficulties across the business community.

As an added incentive for voluntary participation, the government has agreed to accelerate tax deductions for businesses demonstrating good faith compliance. Under these enhanced provisions, companies may now claim the full value of capital allowances for information and communication technology equipment purchases in a single financial year, rather than spreading deductions across multiple years. Additionally, expenses incurred for developing, modifying, or customising computer software systems specifically for e-Invoice functionality qualify for accelerated relief. These provisions effectively reduce the upfront investment burden that many businesses—especially smaller operations—face when upgrading their accounting infrastructure.

The financial incentive structure addresses a key grievance among Malaysia's business community. Many enterprises, particularly MSMEs operating on tight margins, have questioned whether the compliance costs of implementing sophisticated e-invoicing systems justified the administrative benefits. By allowing immediate tax relief rather than deferred deductions, the government signals willingness to share the burden of digital transformation and acknowledges that technology adoption requires capital investment that places genuine strain on smaller operators.

Prime Minister Anwar, who concurrently holds the Finance Ministry portfolio, explicitly framed this programme as a cost-reduction measure for micro, small, and medium enterprises. This positioning reflects broader policy concerns about MSME competitiveness and sustainability, particularly as Malaysia seeks to position itself as a digitally advanced economy while ensuring no segment of the business community is left behind by regulatory change. The announcement came amid ongoing discussions about the pace and implementation of government digitalisation initiatives across various sectors.

The Inland Revenue Board has provided multiple channels through which taxpayers can access guidance and submit their voluntary disclosures. Businesses may contact IRB offices located throughout Malaysia, utilise the dedicated e-Invoice helpdesk at 03-8682 8000, engage with the MyInvois Live Chat service, or communicate via email. This multi-channel approach is intended to reduce barriers to participation and ensure that businesses lacking specialist accounting departments or digital expertise can nonetheless navigate the disclosure process effectively.

Crucially, the IRB has emphasised that all voluntary submissions must remain accurate and fully comply with both General and Specific e-Invoice Guidelines. This requirement protects the integrity of the tax system while maintaining the voluntary nature of the programme. The IRB's insistence on compliance standards also signals that amnesty extends only to process failures and timing issues, not to substantive tax obligations or deliberate misrepresentation of transaction values or other material facts.

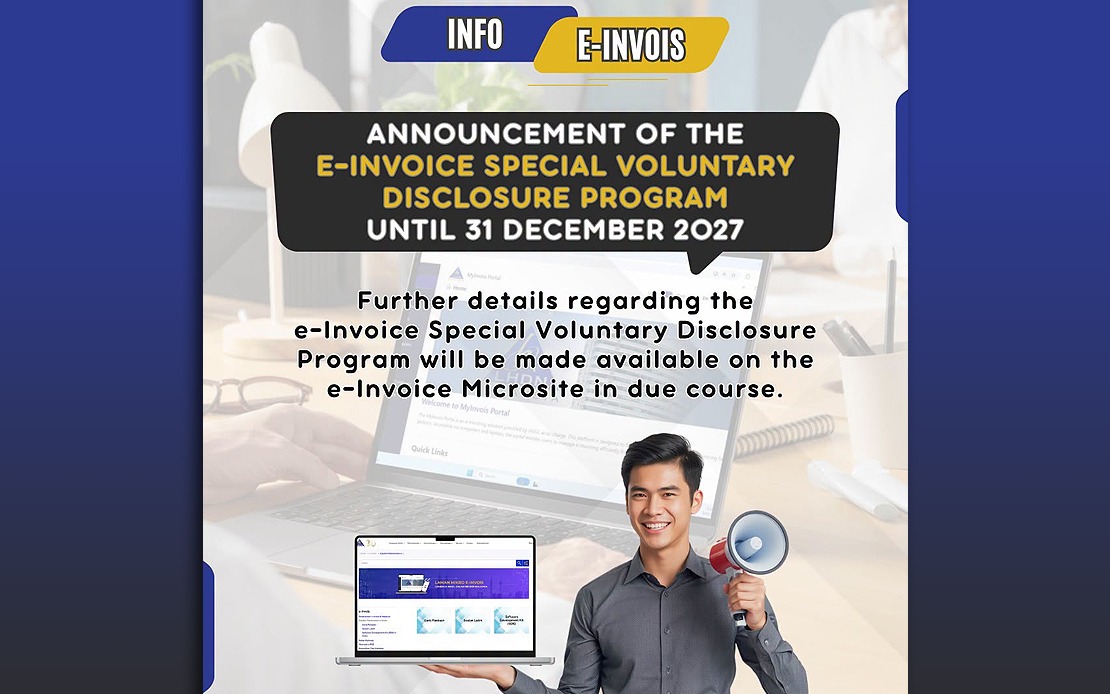

The extended timeline until December 31, 2027, provides businesses with approximately two and a half years to assess their e-Invoice records, identify discrepancies, and submit corrections. This extended window appears designed to reach businesses that may currently be unaware of non-compliance issues or that lack the internal resources to conduct comprehensive compliance audits quickly. The generous timeframe may encourage broader participation than a shorter deadline would achieve, potentially bringing a larger proportion of the business community into full compliance before the amnesty expires.

For Malaysia's business landscape, this programme represents a pragmatic recognition that regulatory change requires adjustment periods and that cooperation often proves more effective than punitive enforcement. The timing also reflects macroeconomic considerations: as the government pursues broader digitalisation and tax modernisation agendas, maintaining business confidence and encouraging voluntary cooperation with new systems serves strategic purposes beyond immediate revenue collection. Businesses that successfully complete the disclosure process will emerge with cleaner compliance records and no accumulated penalties, potentially improving their standing with regulators and lending institutions.

The e-Invoice system itself remains a cornerstone of Malaysia's tax administration modernisation strategy. By requiring businesses to submit invoicing data digitally in real-time or near-real-time, the government gains enhanced visibility into economic activity, improves tax collection efficiency, and creates a more transparent business environment. However, the practical challenges of implementation—particularly for businesses lacking digital infrastructure or technical expertise—have proven more substantial than initial policy assessments anticipated. This disclosure programme tacitly acknowledges those implementation realities while maintaining the system's fundamental objectives.